Monthly gold market and economic insights from Imaru Casanova, Portfolio Manager, featuring her unique views on mining and gold’s portfolio benefits.

Mixed News Drives Flat Prices in May

After reaching a new all-time high in May, offsetting forces kept gold unchanged during the month of June. Gold traded as high as $2,376 per ounce on 6 June. On 7 June, gold closed at its monthly low of $2,294 following news that the central bank of China did not buy any gold bullion in May. Global central bank gold buying has been one of the main drivers of this year’s gold rally, with the Chinese central bank behind a large percentage of those purchases. The People’s Bank of China has been reporting bullion purchases since November 2022, 18 consecutive months of buying. The pause in buying likely raised concern among gold market participants that this important driver of gold demand could weaken. In contrast, gold investment demand has been in decline since April 2022, but in June, global holdings of gold bullion backed exchange traded products finally registered inflows, albeit small, after 12 consecutive months of net outflows. Is western investment demand, the main driver of gold rallies historically, staging a comeback?

Gold also gathered some support from inflation readings (May CPI and PCE) that were interpreted by the market as increasing the likelihood of interest rate cuts by the U.S. Federal Reserve (Fed). At the end of June, the market was pricing in two 25 basis point cuts in 2024, compared to only one 25 basis point cut being priced in at the end of May. Lower real interest rates have historically been supportive of higher gold prices. Gold closed at $2,326.75 per ounce on 28 June, essentially unchanged from its 31 May close of $2,327.33.

Rally in Miners Stalls (Despite Positive Outlook)

Gold stocks did not fare quite as well as the metal in June; NYSE Arca Gold Miners Index (GDMNTR)1 and the MVIS Global Juniors Gold Miners Index (MVGDXJTR)2 were down 3.71% and -6.33%, respectively. We are disappointed with this outcome. The lack of investor interest in gold as an asset class in recent years has frequently led to gold stocks underperforming the metal, not only in a declining gold price environment, which is justified, but also in periods of flat or sideways gold price action. There were no sector wide results, updates or any major events that could explain the generally widespread underperformance across the sector. Quite the opposite, in fact. Many companies provided project updates during the month of June that, in aggregate, we viewed as largely positive.

We took the time to catalogue the announcements, news and updates released by the companies in our gold mining universe during the month of June. We logged approximately 45 company releases including: drilling results; completion of debt and equity financing; completion of mergers and acquisitions; new economic studies, as well as maiden resource estimates, and permits and regulatory approvals for several projects; construction updates, including declaration of first gold pour, from several new mines approaching production; mine specific news and production guidance revisions; comprehensive reviews of companies and assets via investor days; and a new life of mine plan for one of the largest gold mines in the world.

Our original assessment, deeming the news flow broadly positive, was supported by our classification of each release as having the potential of being positive/neutral or negative to the outlook of the company. We classified over 40 of the updates as potentially positive/neutral and only 4 as potentially negative. For reference, the negative news included short term production guidance downgrades due to weather/geotechnical related disruptions; and a serious incident at a single asset, junior company (not held by the Strategy) that halted its operations. Fundamentally, in our opinion, any signs of trouble or weakness were significantly outweighed by signs of strength and health of the sector.

A Closer Look at Agnico Eagle’s Detour Lake

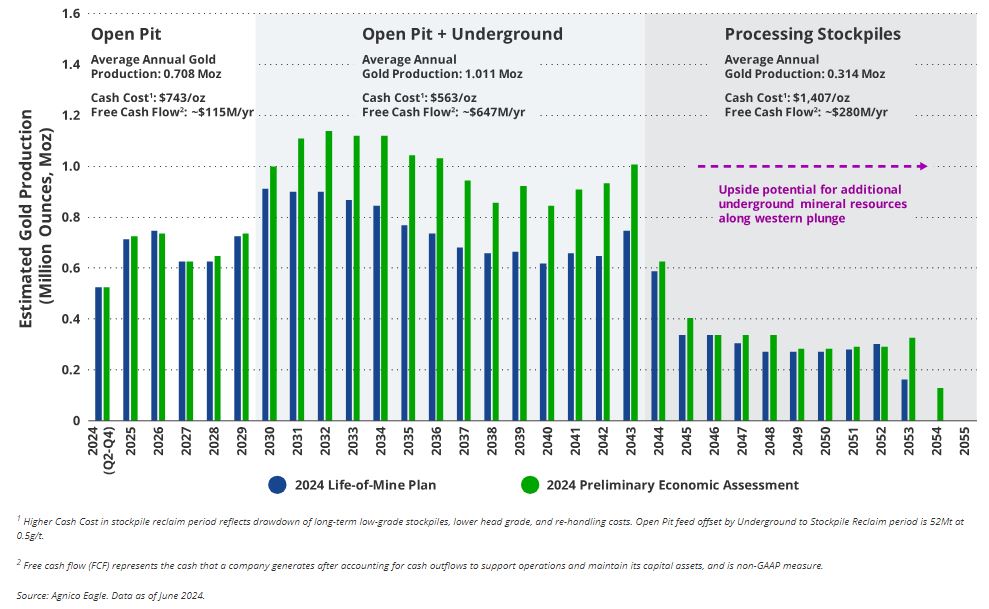

We had the opportunity to visit Agnico Eagle’s (5.01% of Strategy net assets) Detour Lake mine in Ontario. The mine and its potential can certainly be highlighted as a bright spot for the gold industry. We toured the open pit, the processing plant, the tailings dam, the site where the underground exploration ramp portal will be constructed, the maintenance shop and the training center (fleet operating simulator). Overall, our impressions were positive. The mine, the plant and the team showed well. The site visit followed the release of a new life of mine plan and underground project for the asset. The company also hosted a two-hour technical session to review the details of the new plan and project ahead of the site visit. The 2024 plan updates the existing open pit mine production profile and incorporates updated costing. The company has also completed a preliminary economic assessment for a proposed underground mining and mill throughput optimization project, demonstrating the potential to increase the Detour Lake mine's overall production to an average of approximately one million ounces of gold per year over a 14-year period, starting in 2030.

Portfolio Manager Imaru Casanova visiting Agnico Eagle's Detour Lake mine in Ontario.

Annual production is expected to increase to approximately one million ounces per year from 2030 to 2043. This is an increase of approximately 43% or 300,000 ounces of gold annually, when compared to average annual production from 2024 to 2029. From 2044 until 2054, the mine is planned to process stockpile material, producing an average of about 300 thousand ounces of gold per year. Additional exploration has the potential to add ounces to the mine plan in future years and extend the life of the mine beyond 2054. With costs declining as production increases over the next twenty years, the cash flow generation of Detour Lake expands significantly (see chart below). With a pathway to one million ounces, Detour Lake has the potential to move from being one of the 10 largest gold mines in the world, to being one of the top 5 gold mines in the world, in one of the most attractive mining jurisdictions. There is a lot for Agnico Eagle investors to be excited about, providing a great opportunity for Agnico to demonstrate why they are the highest quality gold mining company in the world, and solidify the case behind its historical valuation premium relative to its peers.

Agnico Eagle's "Pathway to One Million Ounce Producer"

To receive more Gold Investing insights, sign up to VanEck's newsletter.